Trying to figure out how much your family health insurance should cost each month can feel confusing and overwhelming. But what if there was a simple way to get a clear estimate tailored just for you and your loved ones?

That’s where the Family Health Premium Calculator comes in. By entering a few key details about your family size, income, and location, you can quickly discover the premium that fits your budget — no guesswork needed. Keep reading to learn how this tool can help you make smarter choices for your family’s health coverage and save money in the process.

Your peace of mind starts here.

How Family Health Premiums Work

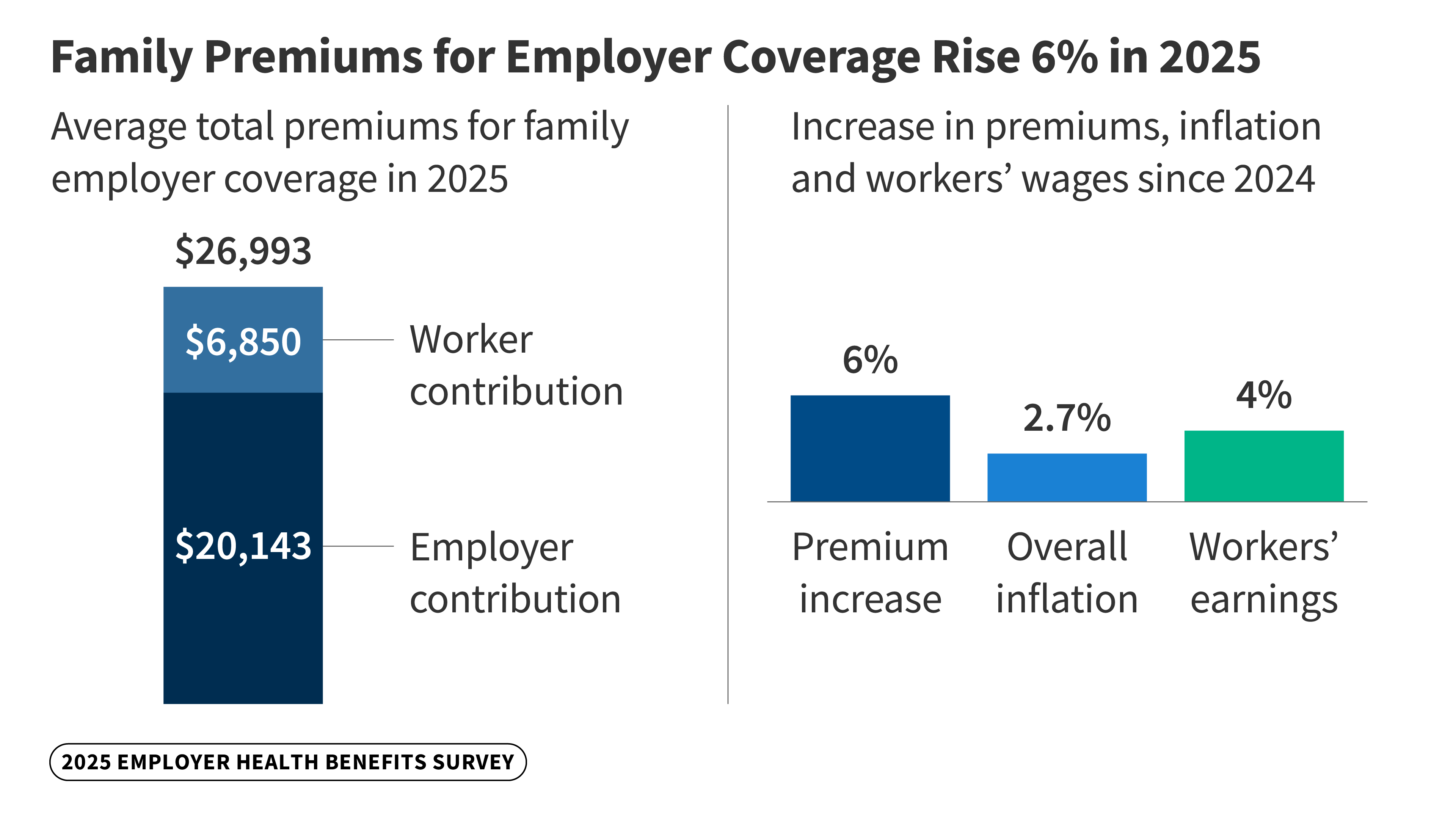

The cost of family health premiums depends on several key factors. Family size plays a major role. Larger families usually pay higher premiums because more people need coverage. Age also affects premiums. Older family members often increase the premium cost due to higher health risks.

Location matters too. Premiums vary widely between regions and states. Areas with higher medical costs tend to have higher premiums. For example, health insurance in urban areas may cost more than in rural locations.

| Factor | Effect on Premium |

|---|---|

| Family Size | More members usually mean higher premiums |

| Age | Older ages raise the cost |

| Region | Premiums differ based on local healthcare costs |

Using A Family Health Premium Calculator

A family health premium calculator needs some basic information to work. This includes the number of family members, their ages, and sometimes the state you live in. These details help estimate the monthly premium cost for your health plan.

Results show the estimated monthly cost and may include subsidy amounts if you qualify. Some calculators also display coverage options and out-of-pocket costs. This helps families compare plans easily.

| Common Features | Description |

|---|---|

| Input Fields | Family size, ages, location, and income details |

| Cost Estimates | Monthly premiums, subsidies, and total costs |

| Plan Comparison | Side-by-side view of different health plans |

| User Friendly | Simple steps and clear results for easy understanding |

Maximizing Savings With Premium Tax Credits

To qualify for premium tax credits, your household income must be between 100% and 400% of the federal poverty level. Family size also affects eligibility. These credits help reduce monthly health insurance costs.

The credit amount depends on the second lowest cost silver plan available in your area. It subtracts a percentage of your household income from the plan’s premium. This lowers the amount you pay out of pocket.

Apply the credits directly to your monthly premiums. This means your insurance company receives the credit, and you pay the rest. You can choose to take the full credit upfront or claim it when filing taxes. This helps manage your family health insurance expenses better.

Estimating Medical And Out-of-pocket Costs

Estimating medical costs starts with predicting healthcare needs. Think about regular doctor visits, prescriptions, and any planned treatments. Family size and ages affect these needs a lot. Using a calculator helps to see future expenses clearly.

Deductibles and copays are important parts of the cost. Deductibles are amounts you pay before insurance helps. Copays are fixed fees for visits or medicine. Both can add up quickly, so include them in your plan.

Unexpected expenses like emergencies or sudden illnesses can be costly. Setting aside money for these surprises is smart. A good health premium calculator lets you plan for all these costs together, making budgeting easier.

Comparing Health Insurance Plans

Plan comparison tools help families find the best health insurance options. These tools show premiums, deductibles, and coverage details side by side. They make it easier to see what each plan offers and at what cost.

Evaluating benefits against costs is key. Some plans have lower monthly premiums but higher out-of-pocket expenses. Others charge more monthly but cover more services with less extra cost. Families should think about their health needs and how often they visit doctors or need prescriptions.

Choosing the right plan means balancing price and coverage. Consider the whole family’s health, budget, and preferred doctors. Look for plans that offer good benefits without too many extra charges. Using a premium calculator can help estimate monthly costs based on family size and ages.

Calculating Household Income For Aca Subsidies

To calculate household income for ACA subsidies, include both taxable and non-taxable income. Non-taxable income can be tax-exempt interest, untaxed Social Security benefits, and foreign income not taxed in the U.S. This full income count helps the government decide subsidy levels fairly.

Adjust income for changes like new jobs or expected raises. If income rises or falls, subsidy amounts may change too. Reporting income changes quickly keeps subsidy amounts accurate.

| Income Type | Examples |

|---|---|

| Taxable Income | Wages, salaries, tips, interest, dividends |

| Non-Taxable Income | Tax-exempt interest, untaxed Social Security, foreign income |

Subsidy amounts depend on your total income. Higher income usually means lower subsidies. Lower income can increase subsidy help. Changes in income require prompt updates to keep subsidies correct.

Tips To Save Big On Family Health Coverage

Choosing the right coverage level saves money and fits your family’s needs. Pick a plan with benefits that cover your usual doctor visits and prescriptions. Avoid paying for extra features you don’t need. A lower deductible plan costs more monthly but less when you visit doctors.

Utilizing employer-sponsored plans can cut costs significantly. These plans often have lower premiums because employers pay part of the cost. Check what your job offers and compare it to other plans. Use the employer plan if it fits your family’s health needs well.

Reviewing and updating coverage annually keeps costs low and benefits up to date. Your family’s health needs may change each year. Look for new plan options during open enrollment. Update your coverage if someone in your family has new health needs or if prices change.

Frequently Asked Questions

How Much Should Family Health Insurance Cost Per Month?

Family health insurance costs vary widely but typically range from $400 to $600 per month. Factors include location, family size, and coverage level. Use online premium calculators to get accurate estimates based on your specific situation and age.

How To Calculate Premium Tax Credit?

Calculate premium tax credit by subtracting a percentage of your household income from the second lowest cost silver plan premium. Use your family size and income details for accuracy.

How To Estimate Medical Costs?

Estimate medical costs by comparing insurance premiums, deductibles, copayments, and out-of-pocket limits. Use online calculators for accuracy. Include expected treatments and prescription expenses to refine estimates.

How To Calculate Income For Aca Subsidy?

Calculate ACA subsidy income by adding your modified adjusted gross income (MAGI), including wages, tax-exempt interest, and untaxed benefits. Count all household members’ incomes expected for the year. Use this total to determine eligibility and subsidy amount on the Health Insurance Marketplace.

Conclusion

Using a Family Health Premium Calculator helps you plan your budget well. It shows clear costs based on your family size and income. You can compare plans side by side to find what fits best. This tool saves time and avoids surprises in your monthly expenses.

Knowing your premium early gives peace of mind for your family’s health needs. Try the calculator today to make smart, informed choices for your coverage.

Read More

- Exclusive Insurance Quote Online: Unlock Instant Savings Today

- Premium Health Insurance Plans: Unlock Ultimate Coverage Benefits

- Sports Car Insurance Rates: Save Big with Expert Tips Today

- Luxury Car Insurance Premium: How to Slash Your Costs Today

- High Net Worth Life Insurance: Essential Strategies for Wealth Protection

- Premium Auto Insurance Quotes: Save Big with Expert Tips Today

- Best Premium Policy Rates: Unlock Top Savings Today

- Executive Vehicle Insurance Quote: Get Instant, Affordable Coverage Today

- Estate Planning Insurance Policy: Essential Tips for Secure Futures

- Premium Life Insurance Quote: Unlock Affordable Coverage Today