Looking for the best premium policy rates can feel overwhelming, especially when every dollar counts. You want coverage that fits your needs without breaking the bank.

But how do you find a policy that offers real value and peace of mind? This article will guide you through the top options, helping you understand what influences premium costs and how you can secure the best rates for your situation.

Keep reading to discover insider tips and smart choices that make your insurance dollars go further—so you get the protection you deserve at a price you can afford.

Top Insurance Providers

Affordable insurance comes from trusted companies known for value. State Farm, Guardian, and Ladder offer competitive rates for term life insurance. These companies balance cost with reliable coverage.

Seniors often need special insurance plans. USAA and New York Life provide tailored policies with fair pricing for older adults. These plans focus on health and age factors.

| Type of Insurance | Leading Provider | Key Benefit |

|---|---|---|

| Affordable Term Life | State Farm | Low monthly premiums |

| Senior Specialized | USAA | Customized for older adults |

| Term Life Leaders | Guardian | Strong financial backing |

Factors Affecting Premium Rates

Age and health play a big role in premium rates. Younger people usually pay less. Health issues like diabetes or heart disease can raise costs.

Coverage amount and term length also affect prices. Higher coverage means higher premiums. Longer terms often cost more but lock in rates.

Lifestyle and risk assessment are key. Smokers or those with risky jobs pay more. Safe habits can help lower premiums.

Comparing Policy Types

Term life insurance offers low premiums and fixed coverage for a set time. It is simple and affordable, making it a popular choice. This type pays a benefit only if the insured dies during the term.

Whole life insurance lasts for a lifetime and builds cash value. Premiums are higher but stay the same over time. It combines protection with a savings component that grows slowly.

Universal life insurance provides flexible premiums and adjustable death benefits. It also builds cash value based on interest rates. This policy suits those who want control over payments and coverage.

| Policy Type | Key Benefits | Cost |

|---|---|---|

| Term Life | Low premium, fixed term, death benefit only | Lowest |

| Whole Life | Lifetime coverage, builds cash value, fixed premium | Higher |

| Universal Life | Flexible premium, adjustable benefits, cash value growth | Moderate to high |

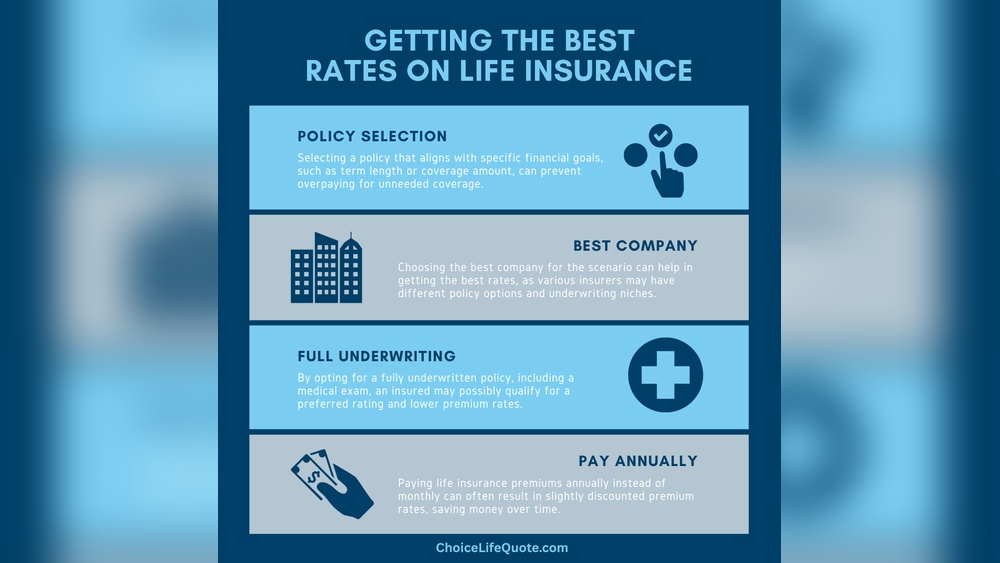

How To Get The Best Rates

Shop and compare quotes from different companies. Use online tools to get quick estimates. Check what each policy covers and its limits. This helps find the best price for your needs.

Improving your risk profile can lower premiums. Keep a good credit score and avoid claims. Install safety devices like alarms and smoke detectors. These steps show you are less risky to insure.

Work with insurance agents who know the market well. They can explain options and suggest discounts. Agents help find policies that fit your budget and coverage needs.

Saving Tips And Tricks

Bundling policies like home and auto can save you a lot. Many companies offer discounts when you buy more than one policy. This often lowers your total premium cost. Ask your insurer about bundle deals before buying.

Choose a coverage level that fits your needs. Too much coverage costs more. Too little leaves you unprotected. Balance price and protection carefully. Check what each plan covers and pick the best match.

Promotions and special offers can lower premiums. Some insurers run discounts for new customers or safe drivers. Keep an eye out for these deals. They can change often, so ask regularly.

Common Myths About Premiums

Cheaper premiums may look good but can mean less coverage. Sometimes, low-cost plans have many hidden fees or poor service. Choosing a plan only by price can cause problems later. It is better to check what is included and how claims are handled.

Preexisting conditions affect your premium rates. Insurers may charge more or deny coverage based on health history. Being honest about your condition avoids claim denials. Some policies offer better terms for certain illnesses.

Age also affects policy availability. Many insurers limit coverage for older people. Younger buyers often get lower rates and more options. Knowing age limits helps pick the right plan early.

Resources For Policyholders

Online quote tools help find and compare policy prices fast. These tools let you enter details once and get quotes from many companies. This saves time and helps spot the best rates easily. Many websites offer free, easy-to-use quote tools.

Financial advice services guide you to choose the right policy. Experts explain complex terms in simple words. They consider your budget, needs, and future plans. Talking to an advisor can prevent costly mistakes and find a plan that fits well.

Consumer protection agencies defend your rights as a policyholder. They handle complaints and offer advice on disputes. These agencies also provide educational materials to help you understand policies better. Checking with them can increase your confidence before buying.

Frequently Asked Questions

How Much Does A $1,000,000 Life Insurance Policy Cost Per Month?

A $1,000,000 life insurance policy typically costs $50 to $200 per month. Rates vary by age, health, and policy type. Younger, healthier individuals pay less. Term life insurance offers lower premiums than whole life policies. Always compare quotes from top insurers for the best rate.

Which Insurance Company Has The Cheapest Premium?

USAA, State Farm, and Guardian often offer some of the cheapest life insurance premiums. Costs vary by age, health, and coverage. Term life insurance usually provides the most affordable rates with fixed premiums over time. Comparing quotes ensures you find the best deal for your needs.

Can I Get Life Insurance With Lupus?

Yes, you can get life insurance with lupus. Expect higher premiums and thorough medical reviews. Choosing specialized insurers helps.

What Does Colonial Penn Give You For $9.95 A Month?

Colonial Penn offers guaranteed acceptance life insurance for $9. 95 a month. It provides up to $25,000 in coverage with no medical exam required. This plan covers final expenses and burial costs, ensuring peace of mind for seniors aged 50 to 85.

Conclusion

Finding the best premium policy rates takes time and research. Compare quotes from different companies carefully. Consider your coverage needs and budget clearly. Lower rates do not always mean better value. Choose a policy that fits your life situation. Stay informed to make smart insurance decisions.

This helps protect you and your family well. Keep checking rates regularly for the best deals.

Read More

- Exclusive Insurance Quote Online: Unlock Instant Savings Today

- Premium Health Insurance Plans: Unlock Ultimate Coverage Benefits

- Sports Car Insurance Rates: Save Big with Expert Tips Today

- Luxury Car Insurance Premium: How to Slash Your Costs Today

- High Net Worth Life Insurance: Essential Strategies for Wealth Protection

- Premium Auto Insurance Quotes: Save Big with Expert Tips Today

- Executive Vehicle Insurance Quote: Get Instant, Affordable Coverage Today

- Estate Planning Insurance Policy: Essential Tips for Secure Futures

- Premium Life Insurance Quote: Unlock Affordable Coverage Today

- Luxury Asset Insurance Premium: Maximize Protection, Minimize Costs