When you’ve worked hard to build substantial wealth, protecting what you’ve earned becomes essential. High net worth life insurance isn’t just another policy—it’s a powerful tool tailored specifically for people like you who want to secure their legacy, reduce taxes, and ensure their family’s financial future.

Imagine having a strategy that not only provides a tax-free payout to your beneficiaries but also helps you manage estate taxes, support business succession, and grow your wealth with confidence. If you want to discover how to make your life insurance work smarter for you and your unique financial situation, keep reading.

This guide will walk you through the key benefits and strategies designed to maximize your wealth protection.

Life Insurance Types For The Wealthy

Whole life insurance offers fixed premiums and a guaranteed death benefit. It builds cash value over time that grows tax-deferred. Wealthy individuals use it for stable growth and financial control without market risk.

Survivorship policies cover two people, usually spouses. The benefit pays out after the second person passes. This helps transfer wealth to heirs efficiently and lowers premium costs.

Private placement life insurance suits accredited investors. It lets policyholders invest premiums in alternative assets like hedge funds, with tax-deferred growth. This option offers flexibility and potential for higher returns.

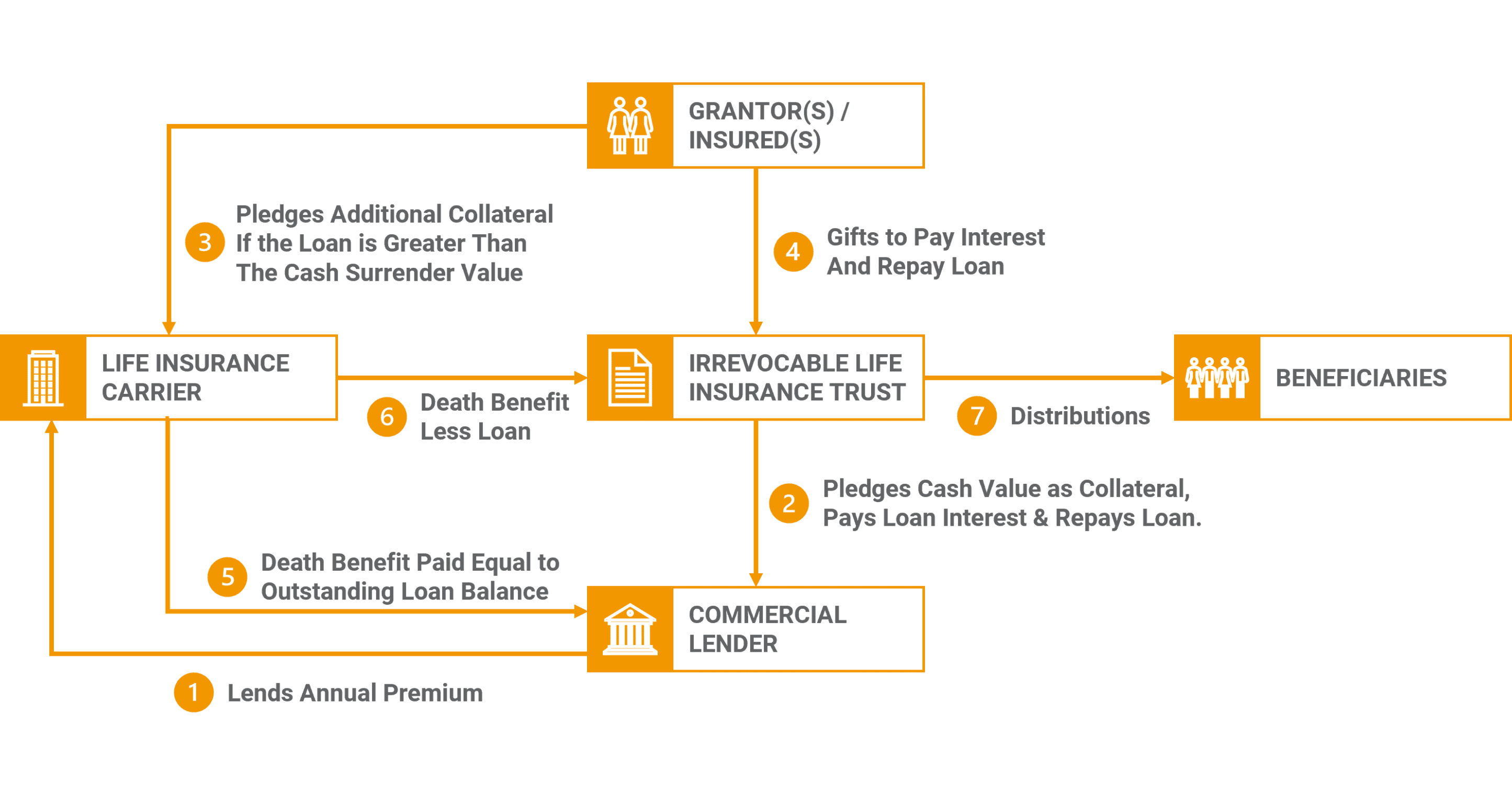

Premium financed life insurance allows wealthy clients to borrow money to pay premiums. This protects their investments by avoiding liquidation. It is ideal for maintaining liquidity while securing large policies.

Tax Advantages And Estate Planning

Income tax-free death benefits provide heirs with money without federal income tax. This helps families keep more of the payout after the insured person passes away. It also offers peace of mind knowing loved ones receive full support.

Estate tax mitigation strategies reduce taxes on large estates. Wealthy individuals use these strategies to protect their assets from heavy government taxes. This helps pass more wealth to the next generation.

Irrevocable Life Insurance Trusts (ILITs) remove the death benefit from the taxable estate. This protects the payout from estate taxes and creditors. ILITs ensure the insurance money goes directly to beneficiaries without tax loss.

Business succession planning uses life insurance to fund buy-sell agreements. This allows partners to buy out a deceased owner’s shares smoothly. It keeps the business stable and avoids financial struggles during ownership changes.

Wealth Protection Techniques

Asset protection shields your wealth from creditors using specific life insurance tools. Irrevocable Life Insurance Trusts (ILITs) can remove the death benefit from your taxable estate, keeping funds safe from claims. This ensures your beneficiaries receive the full payout without legal issues.

Life insurance policies often build cash value over time. This cash can be borrowed against or used in emergencies, providing liquidity without selling assets. Some policies grow steadily, avoiding the ups and downs of the stock market.

Using life insurance for investment purposes helps diversify your portfolio. Private Placement Life Insurance (PPLI) allows investment in alternative assets with tax-deferred growth. Premium financing lets wealthy individuals pay large premiums by borrowing, preserving other investments.

Customizing Policies For High Net Worth

Tailoring coverage to asset levels means choosing the right policy size and type. High net worth individuals often need larger death benefits and special options like tax advantages. Policies can be customized to protect family wealth and cover estate taxes.

Combining policies can improve protection and flexibility. Using a mix of whole life, term, and survivorship policies helps match different financial goals. This approach can lower costs and increase benefits.

Working with financial advisors is important. They help design policies that fit your financial plan and long-term goals. Advisors also assist in coordinating life insurance with other investments for better results.

Advanced Planning Strategies

Irrevocable Life Insurance Trusts (ILITs) help keep life insurance proceeds out of your taxable estate. This means your heirs get the full benefit without losing money to estate taxes. ILITs also protect funds from creditors, preserving your legacy for future generations.

Using life insurance inside trusts allows you to control how money is given to beneficiaries. Trusts can set rules for when and how heirs receive money. This helps avoid conflicts and ensures long-term financial security.

Borrowing to pay insurance premiums can keep your investments intact. Instead of selling assets, you can use loans to cover costs. This strategy helps maintain your current portfolio while funding valuable life insurance policies.

Common Challenges And Solutions

High premium costs often challenge wealthy individuals seeking life insurance. Choosing policies with flexible payment options can ease this burden. Some opt for premium financing, borrowing to cover large premiums without selling assets.

Regulatory rules vary widely and can be complex. Working with advisors familiar with state and federal laws ensures compliance. Proper planning avoids unexpected tax issues or legal problems.

Policy pitfalls include hidden fees, unclear terms, and insufficient coverage. Careful review of policy details prevents surprises. Selecting trusted insurers with transparent contracts is vital. Regular policy checkups keep coverage aligned with changing needs.

Frequently Asked Questions

What Does Dave Ramsey Say About Lirp?

Dave Ramsey advises against using Life Insurance Retirement Plans (LIRPs). He prefers investing in mutual funds and avoiding complex insurance products.

What Kind Of Life Insurance Do The Wealthy Use?

Wealthy individuals prefer whole life, private placement, survivorship, and premium-financed policies for tax benefits, wealth growth, and estate planning.

Can I Get Life Insurance If I Have Cirrhosis?

Life insurance is possible with cirrhosis but often comes with higher premiums or coverage limits. Approval depends on disease severity and treatment. Some insurers may require medical exams or offer limited policies. Consulting specialized agents improves chances of finding suitable coverage.

How Much Does A $1,000,000 Life Insurance Policy Cost Per Month?

A $1,000,000 life insurance policy typically costs $50 to $200 monthly. Costs vary by age, health, and policy type.

Conclusion

High net worth life insurance offers unique benefits for wealth protection. It helps reduce taxes and supports smooth wealth transfer. Many wealthy individuals use permanent policies for long-term planning. Choosing the right policy suits your financial goals best. Speak with a knowledgeable advisor to explore options.

Protect your legacy and ensure your family’s future. Thoughtful planning today brings peace of mind tomorrow.

Read More

- Exclusive Insurance Quote Online: Unlock Instant Savings Today

- Premium Health Insurance Plans: Unlock Ultimate Coverage Benefits

- Sports Car Insurance Rates: Save Big with Expert Tips Today

- Luxury Car Insurance Premium: How to Slash Your Costs Today

- Premium Auto Insurance Quotes: Save Big with Expert Tips Today

- Best Premium Policy Rates: Unlock Top Savings Today

- Executive Vehicle Insurance Quote: Get Instant, Affordable Coverage Today

- Estate Planning Insurance Policy: Essential Tips for Secure Futures

- Premium Life Insurance Quote: Unlock Affordable Coverage Today

- Luxury Asset Insurance Premium: Maximize Protection, Minimize Costs